1926 4th St NE, Washington, DC 20002 | harriethawkins.igoldenonerealty.com | MLS# DCDC2000828

**Home Has Been Appraised At Sales Price** **Closing Considered With Full Price Offer !! Beautiful Traditional Brick Row House in the sought after area of Eckington, 4 Bedrooms, 3 Full Baths, , Living Room, Galley Kitchen with Mud Room attached, Bonus Room off of Formal Dining Room, Fully Finished Basement with storage and enclosed Backyard, New Floors, Remodeled Bathrooms, New Appliances, Close to Rhode Island Row where restaurants, retail stores and the upcoming Rhode Island Avenue Redevelopment is under way, the metro rail and public transportation is within walking distance and just 15 minutes from DOWN TOWN DC THIS IS A MUST SEE

https://harriethawkins.igoldenonereal...

https://youtu.be/fGJEGxSBTc4

https://kerrywoods.blogspot.com/2021/...

Real stories and guidance for Maryland homeowners dealing with probate, pre-foreclosure, vacant property, and difficult selling situations. “Visit MarylandHousePros.com”

Wednesday, September 1, 2021

Monday, August 16, 2021

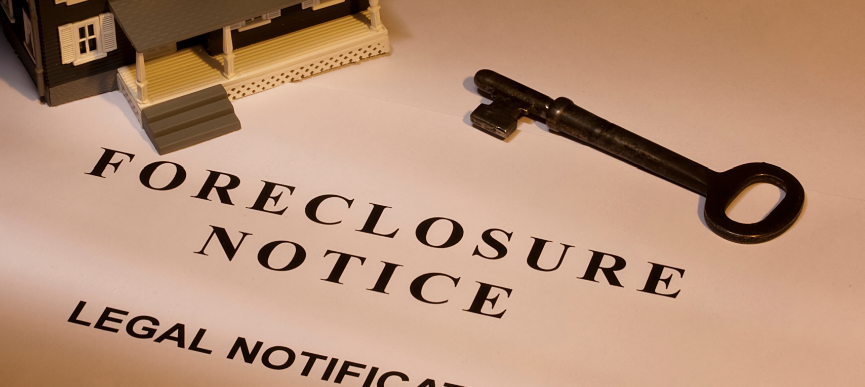

Foreclosure notice of default in Maryland, DC and Virginia– what is it?

If you’ve gotten a foreclosure notice of default and want to know what the heck is going on, keep reading.

Basically, a foreclosure notice of default is a document that has to be filed by a lender to start the process of foreclosure.

The foreclosure notice of default must be sent to anyone who has an interest in the property (any other loans, lenders, or even contractors who are owed money for work done to a property will get a copy).

The foreclosure notice of default must also be published in a newspaper and physically posted in a prominent place on the property itself.

Although this can be really embarrassing to someone going through foreclosure, it’s actually a very important protection for consumers.

Back before US law required a notice of default, people were sometimes foreclosed on without any warning.

In fact, it’s happened even in the past few years – at least one bank has accidentally foreclosed on the wrong property and kicked people out of their house without due process or warning. It’s even happened around Upper Marlboro.

The notice of default is a very important step within the foreclosure process that gives people with an interest in the property to step forward and claim their rights – before it’s too late.

If you’ve received a notice of default, don’t wait. Time is definitely of the essence, and you should take action.

Here are a few key steps you should take:

1) Stay calm and don’t panic.

This may sound obvious, but it’s probably the most important. Anyone in foreclosure is dealing with a lot of stress beyond just the property. These situations don’t happen overnight, and they take a while to solve. You’ll get through it by practicing good coping techniques and taking good care of yourself and your family. Panic leads to bad decisions, so stay cool.

2) Educate yourself.

Learn everything you can about the foreclosure process in your state so that you know what’s happening and what’s coming up next.

3) Gather your resources.

There’s also many non-profit and government resources available out there. You’ll want good legal and tax advice along the way. Definitely don’t try to do it all yourself. This stuff is super complicated with lots of rules.

4) Learn your options.

We’re here to help you avoid foreclosure. We buy houses with cash. We can help you with short sales and even rent-back situations so you (potentially) may be able to keep living in your home. There are many more options than you think.

5) Communicate.

The banks involved don’t want your property. They want money, and what you say matters a lot. You can slow down or stop the foreclosure process if you take the appropriate action.

Want to know more?

Call us anytime (240) 389-4319 or connect with us on our website

and we’ll lay out all of your options for your specific situation.

Friday, July 23, 2021

FEDERAL HOUSING ADMINISTRATION ANNOUNCES ADDITIONAL COVID-19 RECOVERY OPTIONS FOR HOMEOWNERS

| HUD No. 21-115 HUD Public Affairs (202) 708-0685 | FOR RELEASE Friday July 23, 2021 |

FEDERAL HOUSING ADMINISTRATION ANNOUNCES ADDITIONAL COVID-19 RECOVERY OPTIONS FOR HOMEOWNERS

Streamlined COVID-19 Recovery “waterfall” includes broader payment reductions for those most in danger of losing their homes due to COVID-19 financial hardships

WASHINGTON - The Federal Housing Administration (FHA) on July 23, 2021 announced streamlined COVID-19 Recovery options to help homeowners with FHA-insured mortgages who have been financially impacted by the COVID-19 pandemic bring their mortgage current and remain in their homes. The simplified COVID-19 Recovery waterfall allows mortgage servicers to offer eligible homeowners who cannot resume making their mortgage payments a reduction in the principal and interest portion of their monthly payments. The changes announced today will provide those most in danger of losing their homes a path to deep and sustained recovery, including lower income individuals, families of color, and young, first-time homeowners who have disproportionately suffered economic hardships due to the pandemic.

For homeowners who can resume making their existing monthly mortgage payments, FHA has established a revised COVID-19 Recovery Standalone Partial Claim.

Additionally, FHA is reinforcing today that President Biden’s American Rescue Plan Homeowner Assistance Funds (HAF), administered to the States by the Department of Treasury, may be used in connection with FHA-insured mortgages or subordinate mortgages as permitted by the jurisdiction’s HAF program and other requirements.

“Immediately upon taking office, President Biden prioritized the nation’s public health and economic crises by passing the American Rescue Plan,” said Housing and Urban Development Secretary Marcia L. Fudge. “As Americans get back to work and our economy continues to recover, we are taking targeted steps to make sure homeowners impacted financially by COVID-19 have the support they need to remain in their homes. Housing affordability is at its worst and losing your home now would devastate households. These options for FHA borrowers will ensure equitable relief and recovery to people who need it most.”

New COVID-19 Recovery Waterfall

The new FHA COVID-19 Recovery waterfall streamlines and revises FHA’s previous options for struggling homeowners, reduces required documentation, and allows mortgage servicers to provide greater payment reduction for eligible homeowners with FHA-insured Single Family Title II forward mortgages. The simple two-step waterfall options intended for properties that are occupied as the homeowner’s primary residence are:

- COVID-19 Recovery Standalone Partial Claim: for homeowners who can resume making their current mortgage payments, the COVID-19 Recovery Standalone Partial Claim allows mortgage payment arrearages to be placed in a zero interest subordinate lien against the property that is repaid when the mortgage terminates, usually when the homeowner refinances or sells the home.

- COVID-19 Recovery Modification: for homeowners who cannot resume making their current monthly mortgage payments, the COVID-19 Recovery Modification extends the term of the mortgage to 360 months at a fixed rate and targets reducing the borrower’s monthly principal and interest portion of their monthly mortgage payment. The COVID-19 Recovery Modification must include a Partial Claim if the homeowner has Partial Claim funds available.

For properties that are not occupied by the owner, mortgage servicers must offer eligible homeowners FHA’s COVID-19 Recovery Non-Occupant Loan Modification, which extends the term of the mortgage to 360 months, or less if requested by the homeowner, at a fixed interest rate.

“This next step in the evolution of FHA’s COVID-19 response is a significant and meaningful way to help those homeowners who will be at a critical point in their recovery in the coming months and transitioning out of forbearance to permanent sustainable payments,” said Principal Deputy Assistant Secretary for FHA and the Office of Housing Lopa Kolluri. “We can help more homeowners who, through no fault of their own, continue to feel the financially impacts of the pandemic and are unable to make their previous mortgage payment amount. Deeper payment reduction is greatly needed for many of these homeowners to stay in their homes.

COVID-19 Recovery Waterfall Implementation and Homeowner Assessments

Servicers may begin offering the new COVID-19 Recovery waterfall as soon as operationally feasible but must begin using the new waterfall for eligible homeowners within 90 days. In addition, servicers must re-review homeowners for the new COVID-19 Recovery options in circumstances where an existing home retention option has not been completed, where the homeowner was previously ineligible for a COVID-19 home retention option, or if the homeowner has re-defaulted after a COVID-19 home retention option.

“FHA and mortgage servicers have a shared goal of helping as many homeowners as possible to return to sustainable homeownership, and the FHA team will continue to monitor closely the performance of our loss mitigation options to ensure that our policies successfully meet the needs of homeowners impacted by COVID-19,” said FHA Deputy Assistant Secretary for Single Family Housing Julienne Joseph.

The COVID-19 Advance Loan Modification

The changes announced today work in tandem with the pre-waterfall FHA COVID-19 Advance Loan Modification (COVID-19 ALM) announced on June 25, 2021. The COVID-19 ALM requires mortgage servicers to review their FHA mortgage servicing portfolio and offer the COVID-19 ALM to eligible homeowners. Homeowners who choose to accept the COVID-19 ALM need to only review and sign and return the mortgage modification documents sent to them by their mortgage servicer.

Important Information for Homeowners

FHA urges those who are behind on their mortgage payments or are having difficulty complying with the terms of their reverse mortgage or Home Equity Conversion Mortgage (HECM), and have not yet contacted their mortgage servicer, to do so immediately. By contacting their servicer, homeowners can obtain a mortgage payment forbearance or a HECM extension. For FHA forward mortgages, FHA also urges homeowners to engage with their mortgage servicer when their mortgage servicer contacts them about the new COVID-19 ALM or how to bring their mortgage current. Homeowners who are seeking more information on the options available to them should also consider contacting a HUD-approved housing counseling agency.

Thursday, July 22, 2021

Thursday, April 22, 2021

The Postal Service is running a 'covert operations program' that monitors Americans' social media posts

The Postal Service is running a 'covert operations program' that monitors Americans' social media posts

The law enforcement arm of the U.S. Postal Service has been quietly running a program that tracks and collects Americans’ social media posts, including those about planned protests, according to a document obtained by Yahoo News.

The details of the surveillance effort, known as iCOP, or Internet Covert Operations Program, have not previously been made public. The work involves having analysts trawl through social media sites to look for what the document describes as “inflammatory” postings and then sharing that information across government agencies.

“Analysts with the United States Postal Inspection Service (USPIS) Internet Covert Operations Program (iCOP) monitored significant activity regarding planned protests occurring internationally and domestically on March 20, 2021,” says the March 16 government bulletin, marked as “law enforcement sensitive” and distributed through the Department of Homeland Security’s fusion centers. “Locations and times have been identified for these protests, which are being distributed online across multiple social media platforms, to include right-wing leaning Parler and Telegram accounts.”

A number of groups were expected to gather in cities around the globe on March 20 as part of a World Wide Rally for Freedom and Democracy, to protest everything from lockdown measures to 5G. “Parler users have commented about their intent to use the rallies to engage in violence. Image 3 on the right is a screenshot from Parler indicating two users discussing the event as an opportunity to engage in a ‘fight’ and to ‘do serious damage,’” says the bulletin.

“No intelligence is available to suggest the legitimacy of these threats,” it adds.

The bulletin includes screenshots of posts about the protests from Facebook, Parler, Telegram and other social media sites. Individuals mentioned by name include one alleged Proud Boy and several others whose identifying details were included but whose posts did not appear to contain anything threatening.

“iCOP analysts are currently monitoring these social media channels for any potential threats stemming from the scheduled protests and will disseminate intelligence updates as needed,” the bulletin says.

The government’s monitoring of Americans’ social media is the subject of ongoing debate inside and outside government, particularly in recent months, following a rise in domestic unrest. While posts on platforms such as Facebook and Parler have allowed law enforcement to track down and arrest rioters who assaulted the Capitol on Jan. 6, such data collection has also sparked concerns about the government surveilling peaceful protesters or those engaged in protected First Amendment activities.

When contacted by Yahoo News, civil liberties experts expressed alarm at the post office’s surveillance program. “It’s a mystery,” said University of Chicago law professor Geoffrey Stone, whom President Barack Obama appointed to review the National Security Agency’s bulk data collection in the wake of the Edward Snowden leaks. “I don’t understand why the government would go to the Postal Service for examining the internet for security issues.”

The Postal Service has had a turbulent year, facing financial insolvency and allegations that its head, Postmaster General Louis DeJoy, who was appointed by President Donald Trump, was slowing down deliveries just as the pandemic vastly increased the number of mail-in ballots for the 2020 election. Why the post office would now move into social media surveillance, which would appear to have little to do with mail deliveries, is unclear.

“This seems a little bizarre,” agreed Rachel Levinson-Waldman, deputy director of the Brennan Center for Justice’s liberty and national security program. “Based on the very minimal information that’s available online, it appears that [iCOP] is meant to root out misuse of the postal system by online actors, which doesn’t seem to encompass what’s going on here. It’s not at all clear why their mandate would include monitoring of social media that’s unrelated to use of the postal system.”

Levinson-Waldman also questioned the legal authority of the Postal Service to monitor social media activity. “If the individuals they’re monitoring are carrying out or planning criminal activity, that should be the purview of the FBI,” she said. “If they’re simply engaging in lawfully protected speech, even if it’s odious or objectionable, then monitoring them on that basis raises serious constitutional concerns.”

The U.S. Postal Inspection Service did not respond to specific questions sent by Yahoo News about iCOP, but provided a general statement on its authorities.

“The U.S. Postal Inspection Service is the primary law enforcement, crime prevention, and security arm of the U.S. Postal Service,” the statement said. “As such, the U.S. Postal Inspection Service has federal law enforcement officers, Postal Inspectors, who enforce approximately 200 federal laws to achieve the agency’s mission: protect the U.S. Postal Service and its employees, infrastructure, and customers; enforce the laws that defend the nation's mail system from illegal or dangerous use; and ensure public trust in the mail.”

“The Internet Covert Operations Program is a function within the U.S. Postal Inspection Service, which assesses threats to Postal Service employees and its infrastructure by monitoring publicly available open source information,” the statement said.

“Additionally, the Inspection Service collaborates with federal, state, and local law enforcement agencies to proactively identify and assess potential threats to the Postal Service, its employees and customers, and its overall mail processing and transportation network. In order to preserve operational effectiveness, the U.S. Postal Inspection Service does not discuss its protocols, investigative methods, or tools.”

The Postal Service isn’t the only part of government expanding its monitoring of social media. In a background call with reporters last month, DHS officials spoke about that department’s involvement in monitoring social media for domestic terrorism threats. “We know that this threat is fueled mainly by false narratives, conspiracy theories and extremist rhetoric read through social media and other online platforms,” one of the officials said. “And that's why we're kicking off engagement directly with social media companies.”

DHS is coordinating with “civil rights and civil liberties colleagues, as well as our private colleagues, to ensure that everything we're doing is being done responsibly and in line with civil rights and civil liberties and individual privacy,” the official added.

Stone, the University of Chicago professor, questioned why the post office would be tasked with something like identifying violent protests two months after the Jan. 6 attack, which would appear to have little or nothing to do with the post office’s role in delivering mail. “I just don’t think the Postal Service has the degree of sophistication that you would want if you were dealing with national security issues of this sort,” he said.

“That part is puzzling,” he added. “There are so many other federal agencies that could do this, I don’t understand why the post office would be doing it. There is no need for the post office to do it — you’ve got FBI, Homeland Security and so on, so I don’t know why the post office is doing this.”

Friday, February 26, 2021

Federal judge rules eviction moratorium is unconstitutional

Federal judge rules eviction moratorium is unconstitutional

(CNN) A federal judge in Texas on Thursday ruled that the federal moratorium on evictions is unconstitutional, according to court documents.

US District Judge John Barker, who was appointed by then-President Donald Trump to the court in the Eastern District of Texas, stopped short of issuing a preliminary injunction, but said he expected the US Centers for Disease Control and Prevention to respect his ruling and withdraw the moratorium.

"The federal government cannot say that it has ever before invoked its power over interstate commerce to impose a residential eviction moratorium. It did not do so during the deadly Spanish Flu pandemic. Nor did it invoke such a power during the exigencies of the Great Depression. The federal government has not claimed such a power at any point during our Nation's history until last year," Barker wrote.

Although the Covid-19 pandemic persists, he said, "so does the Constitution."

Sunday, February 14, 2021

5 Surprising Things You May Not Know About Working With a Direct Buyer to Sell Your House in DC, Maryland and Virginia

When it is time to sell, hold the phone! Do not automatically jump to reaching out to a real estate agent to begin the traditional listing process. There is a better option than going it alone! As with every other industry, the methods available to sell homes have evolved, leading to direct buyers like Maryland House Pros, LLC in DC, Maryland and Virginia . We will cover five surprising things you may not know about working with a direct buyer to sell your house in DC, Maryland and Virginia.

No Showings

Showings can be the worst part of listing a home. Homes listed on the market, and everything within them, are available for anyone on the internet to view. If having people walking through your home in person or virtually is something you would rather skip. By working with a direct buyer to sell your house in DC, Maryland and Virginia you do not have to worry about scheduling showings, keeping your home ready for showings every moment of the day, and continuously having your weekends or dinner time interrupted.

We Buy As-Is

Prepping a home for a traditional real estate listing can be a great deal of work and expense. An agent will also order an inspection. There may be major repairs that require completion before closing, which come out of your pocket. Unless your home is in perfect or near-perfect condition, handing over the risks, costs, and hassles of repairs by working with a direct buyer to sell your house in DC, Maryland and Virginia makes more sense, and you won’t even have to clean up before you leave.

We Pay Great Prices

Something you may not be aware of is that you will get a fair price by working with a direct buyer like Maryland House Pros, LLC to sell your house in DC, Maryland and Virginia A direct buyer like Maryland House Pros, LLC will offer incredibly fair prices and takes the time to explain our process thoroughly. When you agree that the price is fair, you can be confident that the offer is the actual amount a direct buyer like Maryland House Pros, LLC will pay you in cash.

We Close Fast

With a network of industry professionals behind the scenes, you get an entire team when you work with a direct buyer like Maryland House Pros, LLC to sell your house in DC, Maryland and Virginia is something you may not be aware of. There is no guarantee if your home will sell with a traditional listing, if you face personal or financial adversity that requires you to relocate and you need the cash from your home sale quickly, they can quickly purchase homes and make you an offer on the spot. Because we pay cash, there is no inspection, appraisal, or mortgage lenders red tape to untangle; the majority of deals can close in 30 days or less from the time of the initial meeting!

It’s Easy

The simplicity of working with a direct buyer to sell your house in DC, Maryland and Virginia is something you may not be aware of. Our contracts are straightforward, and we walk you step by step through the process, explaining every step of the way, without all of the complications of listings. There is no stress, and there are no commissions for you to try to avoid by taking on all of the expenses, responsibilities, and risks of selling on your own.

Maryland House Pros, LLC makes selling homes as easy as pie, saving your time and money! Maryland House Pros, LLC is happy to answer any questions you may have about working with a direct buyer and the many surprising things you may not know about working with a direct buyer to sell your house in DC, Maryland and Virginia Why not send us a message or call Maryland House Pros, LLC at (240) 389-4319 for your offer right now!

Saturday, February 6, 2021

The diverse history of Historically Black Colleges and Universities.

The diverse history of Historically Black Colleges and Universities.

While Jewish and African American communities have a tumultuous shared history when it comes to the pursuit of civil rights, there is a chapter that is often overlooked. In the 1930s when Jewish academics from Germany and Austria were dismissed from their teaching positions, many came to the United States looking for jobs. Due to the Depression, xenophobia and rising anti-Semitism, many found it difficult to find work, but more than 50 found positions at HBCUs in the segregated South.

Originally established to educate freed slaves to read and write, the first of the Historically Black Colleges and Universities was Cheyney University in Pennsylvania, established in 1837. By the time Jewish professors arrived, the number of HBCUs had grown to 78. At a time when both Jews and African Americans were persecuted, Jewish professors in the Black colleges found the environment comfortable and accepting, often creating special programs to provide opportunities to engage Blacks and whites in meaningful conversation, often for the first time.

In the years that followed, the interests of Jewish and African American communities increasingly diverged, but this once-shared experience of discrimination and interracial cooperation remains a key part of the Civil Rights Movement.

Image: Melrose Cottage, built in 1805, Cheyney University of Pennsylvania.

Friday, February 5, 2021

One in four cowboys was Black, despite the stories told in popular books and movies.

In fact, it's believed that the real “Lone Ranger” was inspired by an African American man named Bass Reeves. Reeves had been born a slave but escaped West during the Civil War where he lived in what was then known as Indian Territory. He eventually became a Deputy U.S. Marshal, was a master of disguise, an expert marksman, had a Native American companion, and rode a silver horse. His story was not unique however.

In the 19th century, the Wild West drew enslaved Blacks with the hope of freedom and wages. When the Civil War ended, freedmen came West with the hope of a better life where the demand for skilled labor was high. These African Americans made up at least a quarter of the legendary cowboys who lived dangerous lives facing weather, rattlesnakes, and outlaws while they slept under the stars driving cattle herds to market.

While there was little formal segregation in frontier towns and a great deal of personal freedom, Black cowboys were often expected to do more of the work and the roughest jobs compared to their white counterparts. Loyalty did develop between the cowboys on a drive, but the Black cowboys were typically responsible for breaking the horses and being the first ones to cross flooded streams during cattle drives. In fact, it is believed that the term “cowboy” originated as a derogatory term used to describe Black “cowhands.”

Image: Bass Reeves, The first African-American US Deputy Marshal

Is it Illegal to Purchase a Home In Pre-Foreclosure in the State of Maryland?

Maryland enacted the Protection of Homeowners in Foreclosure Law (PHIFA) which has various rules restricting investors privately approaching homeowners in foreclosure to buy their home.

Q – Is it Illegal to Purchase a Home In Foreclosure in the State of Maryland?

A – NO! The Protection of Homeowners in Foreclosure Act of 2005, also known as (a/k/a) SB-761, and “The Maryland Foreclosure Law”, was passed by the Maryland Legislature and Signed into Law by Governor Ehrlich to protect homeowners from mortgage and foreclosure scams. The law specifically allows for Foreclosure Purchasers to purchase homes in foreclosure from homeowners. HOWEVER, the intent of the Legislature was to prevent investors who purchase foreclosures from dealing directly with homeowners and spells out the need for a “Foreclosure Consultant” to assist the homeowner and to provide for a true “arms-length” third-party to protect the interests of the homeowner(s) in dealing with investors seeking to purchase their homes during a time of foreclosure. Foreclosure investing continues to be completely legal (and profitable) for investors; however, it must be done in accordance with the Maryland Law.

Q – How Does One Become a Maryland Foreclosure Consultant?

A – The Protection of Homeowners in Foreclosure Act of 2005, also known as (a/k/a) SB-761, and Maryland Foreclosure Law, spells out specific tasks, which if performed by a person contacting a Maryland homeowner in foreclosure constitute acts of being a “Foreclosure Consultant”. In other words, what you do makes you a Foreclosure Consultant under the law and not necessarily what you put on your business cards. The problem, of course, is that as a “Foreclosure Consultant”, it is against the law to then turn around and purchase the home from the homeowner.

Q – Can I be BOTH a Foreclosure Consultant and a Foreclosure Purchaser?

A - The Protection of Homeowners in Foreclosure Act of 2005, specifically prohibits persons who act as Foreclosure Consultants from also being Foreclosure Purchasers within the same transaction. Unfortunately, the law as is currently written is unclear as to whether a Foreclosure Consultant can also become a Foreclosure Purchaser on different transactions. HOWEVER, the law does go to great lengths to spell out that a Foreclosure Purchaser can not use the services of a Foreclosure Consultant who is a family member, a blood relative, a spouse, or an entity controlled by the Foreclosure Consultant or related persons. In short, the law seeks to place a “WALL” between the Foreclosure Consultant and the Foreclosure Purchaser in an effort to protect the interests of the homeowner. Therefore, it is prudent to pick which side of the fence you want to be on. There is nothing in the law currently, which prohibits a Foreclosure Consultant from becoming a Foreclosure Purchaser in the future.

Q – What are the penalties for breaking the law?

A – Currently the law states that the penalties for infringement are a fine, up to $10,000, per occurrence and up to 3-years in jail, also per occurrence, Note: someone who breaks this law could unknowingly commit multiple occurrences of violating the law on one transaction.

Q – Besides a $10,000 fine [per occurrence] and 3-years jail time [per occurrence] are there any other penalties to be aware of?

A – Yes, in addition to any criminal charges, an investor who violates the law will probably also face a civil suit in one of Maryland’s Circuit Courts. Specifically, In February 2006, Judge Steven I. Platt of the Circuit Court for Prince George's County, Maryland, issued an opinion and order in the case of Tommie Mae Smith v. Vincent Abell that the “investor” pay to the homeowner a $510,983, fine consisting of $10,968 in actual damages – the amount that she spent to pay the attorney for the mortgage company and her own attorney, and $500,000 in punitive damages, which of course was split with her attorney. The Maryland Bar has called civil actions against violators of the law, “An Emerging Area of Consumer Law".

Thursday, February 4, 2021

Inoculation was introduced to America by a slave.

Inoculation was introduced to America by a slave.

Few details are known about the birth of Onesimus, but it is assumed he was born in Africa in the late seventeenth century before eventually landing in Boston. One of a thousand people of African descent living in the Massachusetts colony, Onesimus was a gift to the Puritan church minister Cotton Mather from his congregation in 1706.

Onesimus told Mather about the centuries old tradition of inoculation practiced in Africa. By extracting the material from an infected person and scratching it into the skin of an uninfected person, you could deliberately introduce smallpox to the healthy individual making them immune. Considered extremely dangerous at the time, Cotton Mather convinced Dr. Zabdiel Boylston to experiment with the procedure when a smallpox epidemic hit Boston in 1721 and over 240 people were inoculated. Opposed politically, religiously and medically in the United States and abroad, public reaction to the experiment put Mather and Boylston’s lives in danger despite records indicating that only 2% of patients requesting inoculation died compared to the 15% of people not inoculated who contracted smallpox.

Onesimus’ traditional African practice was used to inoculate American soldiers during the Revolutionary War and introduced the concept of inoculation to the United States.

Wednesday, February 3, 2021

Little Known Black History Fact

Before there was Rosa Parks, there was Claudette Colvin.

Most people think of Rosa Parks as the first person to refuse to give up their seat on a bus in Montgomery, Alabama. There were actually several women who came before her; one of whom was Claudette Colvin.

It was March 2, 1955, when the fifteen-year-old schoolgirl refused to move to the back of the bus, nine months before Rosa Parks’ stand that launched the Montgomery bus boycott. Claudette had been studying Black leaders like Harriet Tubman in her segregated school, those conversations had led to discussions around the current day Jim Crow laws they were all experiencing. When the bus driver ordered Claudette to get up, she refused, “It felt like Sojourner Truth was on one side pushing me down, and Harriet Tubman was on the other side of me pushing me down. I couldn't get up."

Claudette Colvin’s stand didn’t stop there. Arrested and thrown in jail, she was one of four women who challenged the segregation law in court. If Browder v. Gayle became the court case that successfully overturned bus segregation laws in both Montgomery and Alabama, why has Claudette’s story been largely forgotten? At the time, the NAACP and other Black organizations felt Rosa Parks made a better icon for the movement than a teenager. As an adult with the right look, Rosa Parks was also the secretary of the NAACP, and was both well-known and respected – people would associate her with the middle class and that would attract support for the cause. But the struggle to end segregation was often fought by young people, more than half of which were women.

Image: Claudette Colvin by Phillip Hoose

Saturday, January 23, 2021

States will soon start giving out $25 billion in rental assistance. How to apply

A $25 billion federal rental assistance fund will soon be disbursed to states, allowing those struggling amid the Covid pandemic to apply for the money.

By one estimate, 14 million Americans are behind on their rent during the crisis. Advocates say more rental assistance will be needed to stave off an unprecedented wave of evictions. After 10 months of record job losses and business shutdowns, rental arrears in the U.S. may be closer to $70 billion.

President Joe Biden is calling on Congress to allocate another $30 billion in housing aid, and on his first day in office announced an executive order that will extend the national ban on evictions through March.

For now, here’s what you need to know about accessing funds authorized by the $25 billion Emergency Rental Assistance Program.

Am I eligible?

To qualify for the assistance, at least one member of your household has to have lost income or incurred significant expenses due to the pandemic, or be eligible for unemployment benefits.

You will also need to demonstrate a risk of homelessness. In addition, your income level for 2020 can’t exceed 80% of your area’s median income, though states have been directed to prioritize applicants who fall at 50% or lower, as well as those who’ve been out of work for 90 days or more.

Expect to have to show in writing that you meet these requirements, such as with a past due rent or utility notice.

Are the funds available now?

States will have the funds by Jan. 26.

How do I apply?

“Where or how to apply will vary city by city,”

Many areas have existing rental assistance funds, and it will be through one of these that you apply for the new aid. In other cases, programs will be created to disburse the money.

“Renters should contact local housing groups, their representatives or the local 211/311 lines to identify programs and learn how to apply.

Your landlord can also apply for you but must get your signature and provide you with a copy of the application.

How much could I get?

Renters can get help with up to 12 months of back rent and utility bills, and potentially another three months of support if there’s still money available. In some cases, you can get funds to cover future rent payments, but only if there’s a plan to address any debts first.

The funds are paid directly to your landlord or utility company.

Do I need to be behind on my rent to qualify?

No. But you can’t get money for future rent payments until any rental arrears have been paid off.

Can I apply for money just for utility or energy costs?

Yes.

I’m a homeowner. Can I apply for this assistance?

No. You must be a renter.

I’m facing eviction. What should I do?

Apply for the funds as soon as possible.

Also, understand your rights. Most renters should be allowed to stay in their homes at least through March thanks to a national ban prohibiting evictions for nonpayment of rent.

To evoke that protection, you’ll need to attest on a declaration form that you meet a few requirements, such as expecting to earn less than $99,000 in the 2020-2021 calendar year.

“If a tenant cannot pay the rent, they should provide the declaration to their property owner as soon as possible. In addition to the national eviction ban, some states have issued their own moratoriums, some of which are more comprehensive than the federal law. Get informed about any policies that apply to you.

Last, if your landlord ignores any of these rules, as some are doing, get a lawyer. You can find low-cost or free legal help with an eviction in your state at Lawhelp.org or TPF.Legal

One study in New Orleans found that more than 65% of tenants with no legal representation were evicted, compared with fewer than 15% of those who did have a lawyer in court.

Subscribe to:

Comments (Atom)